DOJ Announces Key Revisions to Corporate Enforcement and Voluntary Self-Disclosure Policy

What You Need To Know

- The U.S. Department of Justice updated its Corporate Enforcement and Voluntary Self-Disclosure Policy (CEP), offering more benefits for firms that voluntarily disclose federal law violations and cooperate with investigations.

- The revised policy provides clearer pathways for companies to secure declination—DOJ's agreement not to seek a criminal resolution, if they meet specific criteria outlined by the department.

- A new “Near Miss” category allows firms that don't meet the criteria for declination to possibly secure a non-prosecution agreement.

On May 12, 2025, the Head of the Department of Justice’s (DOJ) Criminal Division, Matthew Galeotti, announced a new white collar enforcement plan in a memorandum entitled “Focus, Fairness, and Efficiency in the Fight Against White-Collar Crime.” The new memorandum and accompanying public remarks by Galeotti unveiled key changes to the division’s Corporate Enforcement and Voluntary Self-Disclosure Policy (CEP) that provide greater incentives for corporations to investigate and voluntarily self-disclose conduct by employees that violates federal criminal laws and cooperate with DOJ investigations. This alert summarizes these changes to the CEP and assesses how they may impact the calculus for companies that are considering voluntary self-disclosure.

Background

Over the last several years, DOJ has updated and expanded its CEP, requiring every department component, including U.S. Attorney’s Offices, to promulgate and publicize the same. The policies are designed to reward corporations’ full cooperation with the DOJ through self-reporting, timely remediation of criminal conduct, and implementation and testing of effective compliance programs.

Summary of the Criminal Division’s Revised CEP

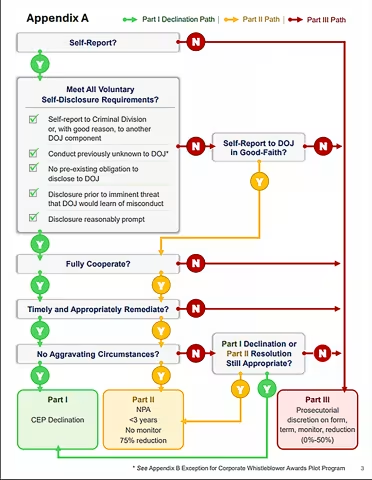

The revised CEP, with corresponding changes to DOJ guidance on monitors and its recently launched Corporate Whistleblower Awards Pilot Program, should result in an easier and clearer path for companies to obtain a declination. It gives companies more definitive guidance that if they meet established criteria they “will” receive a declination—that is, an agreement by DOJ not to seek a criminal resolution.

The prior CEP only provided criteria giving rise to a “presumption” of a declination. “Companies that meet our core requirements . . . will not be required to enter into a criminal resolution,” Galeotti said in announcing the changes. “This is a clear path to declination.”

For the purposes of the CEP, the Criminal Division defines voluntary self-disclosure as follows:

- The company must self-disclose to the Criminal Division, or another DOJ office or component if the ultimate resolution includes the Criminal Division

- The misconduct is not previously known to DOJ

- The company had no preexisting obligation to disclose the misconduct to DOJ

- The voluntary disclosure occurs “prior to an imminent threat of disclosure or government investigation,” as defined in U.S.S.G. § 8C2.5(g)(1)

- The company discloses promptly after becoming aware of the misconduct, with the burden being on the company to demonstrate timeliness

In addition to meeting the criteria for voluntary self-disclosure, the following additional factors must be met:

The company fully cooperated with the Criminal Division’s investigation - The company timely and appropriately remediated the misconduct

- There are no aggravating circumstances related to the nature and seriousness of the offense, egregiousness or pervasiveness of the misconduct within the company, severity of harm caused by the misconduct, or criminal adjudication or resolution within the last five years based on similar misconduct by the entity engaged in the current misconduct

Even in the event of aggravating circumstances, however, under the revised CEP prosecutors “retain the discretion to nonetheless recommend a CEP declination based on weighing the severity of those circumstances and the company’s cooperation and remediation.” As part of the CEP declination, the company will be required to pay all disgorgement/forfeiture and restitution/victim compensation payments resulting from the misconduct at issue.

The revised CEP also introduces the concept of a “Near Miss” voluntary disclosure. Under this “Near Miss” framework, if a company fully cooperated and timely and appropriately remediated, but the company is ineligible for a declination due to (1) the fact that a self-disclosure made in good faith does not meet the definition of a voluntary self-disclosure or (2) “it had aggravating factors that warrant a criminal resolution,” the Criminal Division “shall” nevertheless:

- Provide a non-prosecution agreement, “absent particularly egregious or multiple aggravating circumstances”

- “Allow a term length [for a non-prosecution agreement] of fewer than three years”

- “Not require an independent compliance monitor”

- “Provide a reduction of 75% off the low end of the U.S. Sentencing Guidelines (U.S.S.G.) fine range”

The new “Near Miss” category provides increased incentives for companies to voluntarily self-disclose, even when they do not qualify for the mandatory declination.

Where a company does not self-report the criminal conduct in good faith, it will not be able to avail itself of the above-described benefits. Still, Criminal Division prosecutors retain discretion to recommend a resolution of any form, with a three-year term, monitor, and up to a 50% reduction in the fine.

The revised CEP also includes a flow chart mapping out the potential path to declination:

The revised CEP retains certain key aspects of the prior iteration of the CEP (effective August 1, 2024) in how it overlaps with the Corporate Whistleblower Awards Pilot Program. In particular, the revised CEP retains the following key exception regarding the definition of voluntary disclosure:

“If a whistleblower makes both an internal report to a company and a whistleblower submission to the Department, the company will still qualify for a presumption of a declination under the CEP—even if the whistleblower submits to the Department before the company self discloses—provided that the company: (1) self-reports the conduct to the Department within 120 days after receiving the whistleblower’s internal report; and (2) meets the other requirements for voluntary self-disclosure and presumption of a declination under the policy.”

Key Takeaways

- A clear path, not a presumption. The revised CEP provides companies transparency to understand the incentives for self-disclosure and guarantees that a company that self-reports will receive a declination—not merely a presumption against prosecution—assuming that the company fully cooperates and implements remedial measures, absent aggravating circumstances.

- Even companies that don’t strictly meet all of the voluntary self-disclosure requirements still may attain a non-prosecution agreement (NPA). The new “Near Miss” category makes an NPA more viable even for companies that do not meet all of the requirements for a declination under the CEP.

- Handling of internal whistleblowers remains key. Internal whistleblower reports that are not handled properly could, in certain circumstances, jeopardize a company’s ability to qualify for a declination.

What’s Next?

The revised CEP even more clearly illustrates the benefits of self-reporting and cooperation than its predecessor. Corporations, especially their in-house counsel and compliance officers, should review their existing compliance programs and internal reporting channels and procedures to ensure eligibility for guaranteed declinations.