Key Takeaways from Fenwick's 2019 Digital Health Investor Summit

Fenwick’s eighth annual Digital Health Investor Summit took place against the backdrop of strong and increasingly diverse investment markets, a focus on clinical validation of digital health tools, and a healthcare system that is shifting to prioritize wellness and disease prevention rather than treating diseases only after they have developed. Speakers included Rock Health’s Bill Evans and Goldman Sachs’s Peter van der Goes, who shared the digital health investment outlook for 2020, and Rock Health’s Megan Zweig, who discussed developments in digital health therapeutics with Antoun Nabhan of Pear Therapeutics and Jenna Carl of Big Health. My colleague Dawn Belt moderated a panel on wellness and remote patient monitoring with TRIPP’s Nanea Reeves and Forward’s Adrian Aoun. To finish the day, Fenwick’s Ian Goldstein chatted with Bill Taranto about startup enterprise partnerships in the digital health space.

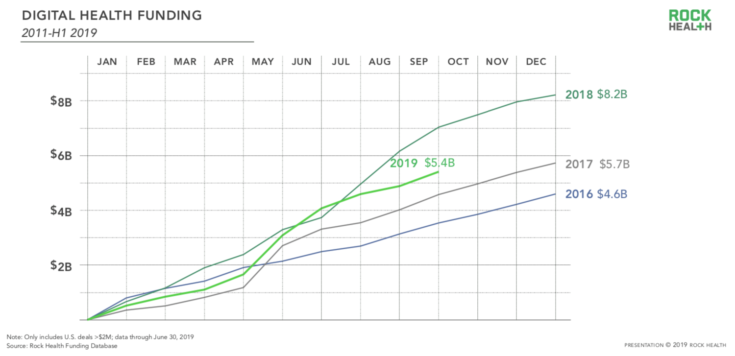

Mega-Rounds Drive Topline Total

Bill Evans, CEO and managing director of Rock Health, kicked off the summit by presenting hot-off-the-presses data on private digital health investment over the third quarter. He reported that investment in the third quarter totaled $1.3 billion, bringing the year-to-date total to $5.4 billion. That puts the sector on pace to bring in about $7.5 billion in 2019, which is just below last year’s record-setting total of $8.1 billion, but still well ahead of 2016 and 2017.

Evans noted that mega-rounds were still the norm through the third quarter, and those deals continue to drive the topline total. The average deal size so far in 2019 has been $20.9 million, down only slightly from $21.7 million in 2018.

Nine companies have closed deals valued at more than $100 million so far in 2019, including three for $200 million or more and one for $300 million (a growth round for Gympass, an employee fitness platform).

Evans reported that through the end of the third quarter in 2019, 262 digital health companies raised more than $2 million.

IPOs Make a Comeback

On the public side, Goldman Sachs’ Peter van der Goes highlighted the triumphant return of the digital health IPO. After a public offering drought over the last two years, 2019 has already seen four digital health IPOs—a large number for the industry—and van der Goes anticipates a few more will be made by the end of the year due to high market demand.

Evans and van der Goes both underscored the difference between the digital health and tech sectors. As van der Goes put it, four IPOs is good, but small when compared to tech, which had 24 in the same period. But Evans noted that investors are coming to understand that digital health companies have a longer incubation period compared to pure tech companies. A more educated investor base will make it easier for digital health companies to access capital through either public or private markets.

According to van der Goes, the diversity of the companies that have gone public this year signals that investors are pursuing strong companies rather than chasing trending technologies. The class of 2019 includes: Health Catalyst (a data analytics company), Change Healthcare (a healthcare technology company), Livongo (a chronic disease management platform) and Phreesia (a patient intake platform). He noted that these companies also vary significantly in terms of revenues, revenue growth, profitability and ownership.

Van der Goes also noted that there has been some volatility in the performance of the latest crop of IPOs, owing to macro market conditions. Nevertheless, van der Goes does not expect the post-IPO performance of these companies to put any downward pressure on demand.

On the M&A side, van der Goes reported a robust year, with the value of M&A activity in 2019 totaling $25.6 billion so far. That compares favorably to an average of $16.5 billion a year from 2015 through 2018. The number of deals (valued at more than $1 billion) also increased significantly to nine in 2019 from an average of five from 2015 through 2018.

Van der Goes also noted that strategic acquirers in the digital health space have come from diverse sectors including not only healthcare services and pharmaceuticals, but also industrial conglomerates and financial technology. He also highlighted the role that private equity capital is playing in digital health M&A and the diversity of these deals, which include classic acquisitions, minority investments and scale/growth equity.

Industry Trends to Watch

Digital Therapeutics

In his presentation, Rock Health’s Evans reported that behavioral health has eclipsed cardiovascular and oncology to rank as the top-funded clinical indication in the first half of 2019. So, it was fitting that our first fireside chat focused on two behavioral health companies. Rock Health’s Megan Zweig talked with Pear Therapeutics’ Antoun Nabhan and Big Health’s Jenna Carl about trends in digital therapeutics.

Nabhan and Carl explained that there is no one-size-fits-all market pathway for digital therapeutics companies. Pear Therapeutics—which discovers, develops and delivers software-based therapeutics—goes to market through the traditional channel of driving prescriptions through physicians. Meanwhile, Big Health, developer of the Sleepio app, markets to large employers who want to increase the productivity and well-being of their employees.

How did the two companies choose their respective approaches to the market? Carl said Big Health’s largest customer is a self-funded employer health plan, so it was a natural fit for the digital therapeutics company to continue to work through employers and avoid dealing with a fragmented health insurance market in the U.S.

On the other hand, Nabhan, who had previously worked in the medical technology sector, said he feels working with physicians provides companies like Pear Therapeutics with a well-defined pathway to patients and payers.

Regardless of market strategy, both Nabhan and Carl agree that clinical data validation is critical to the success of any digital therapeutic. As Nabhan put it, clinical evidence has been crucial in “getting over the hype cycle.” Both agree that clinical data validation will become more important in the coming years.

Wellness and Remote Patient Monitoring

Fenwick’s Dawn Belt moderated a session on wellness and remote patient monitoring with guest panelists Nanea Reeves of TRIPP and Adrian Aoun of Forward.

Reeves and Aoun anticipate remote monitoring will play a key role in changing the way we look at healthcare by encouraging providers and patients to focus on wellness and prevention rather than curative medicine. For example, Aoun says, access to “tons of data” generated on each patient through monitoring will allow providers to better manage patients with chronic conditions or provide an early-warning system for patients with health risks.

Reeves noted that wellness and remote patient monitoring tools are being adapted by the biohacker community, which she thinks is a natural fit. In 20 years, biohacking will be “medicine,” as remote patient monitoring and an emphasis on wellness will be at the center of healthcare services, Reeves said.

A Startup-Enterprise Partnership Case Study

To finish off the day, Fenwick’s Ian Goldstein chatted with Bill Taranto of Merck’s Global Health Innovation Fund (GHI) about how healthtech startups can work with large enterprises.

Taranto highlighted GHI’s investment in Livongo, one of the digital health companies that completed an IPO this year, as a case study. GHI’s investment priorities have shifted to align with Merck’s increasing focus on cancer and diabetes. The investment was a natural fit because Livongo’s focus on diabetes monitoring and detection complemented Merck’s therapeutic priorities.

The lesson? Keep the criteria for investment straightforward: Identify a problem in healthcare, then look for companies that offer a solution to that problem.

What’s Next?

In the short-term, expect to see one or two more digital health IPOs before the end of the year and eight to 10 more in 2020. As Peter van der Goes put it, despite current market volatility, digital health offers a good opportunity for investors who “want to find ways to put money into ventures that take costs out of the [healthcare] system in ways that biotech and medtech don’t.”

In emerging technologies, clinical data validation will become more important for digital therapeutics in the coming years and remote patient monitoring will play a crucial role in transforming traditional healthcare systems. Finally, as tech and healthcare giants make plays in the digital health sector, expect to see more healthtech startups partner with large enterprises to target specific healthcare problems.

Originally published November 20, 2019 on Fenwick's Life Sciences Legal Insights blog.